Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Economy

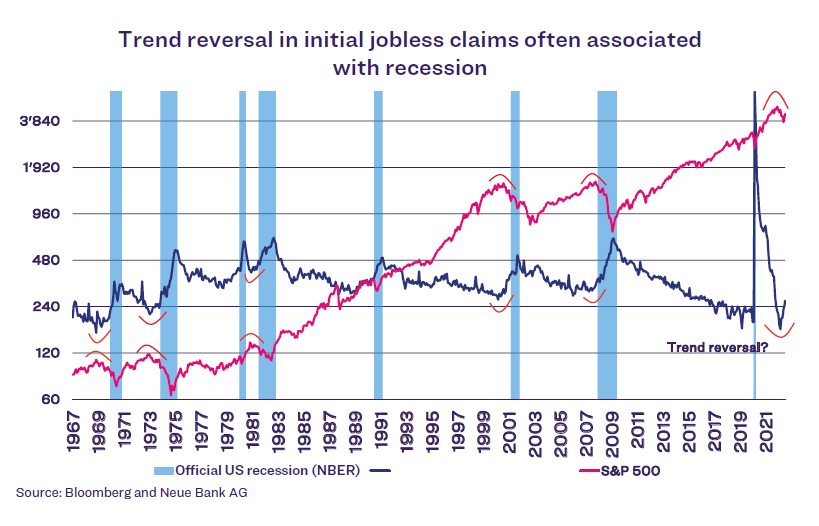

Is a recession coming or are we already in one? This is the crucial question that investors are currently asking themselves. In the United States, the National Bureau of Economic Research (NBER) is responsible for declaring an official recession. Following the motto “with the benefit of hindsight”, the NBER confirms a recession only several months after it has begun. To determine periods of recession, the NBER relies not only on pure GDP figures, but rather on a much broader set of data. The NBER’s analysis also takes into account incomes, corporate earnings, and the state of the labour market. Purely from a GDP perspective, the US would already be in a recession, given that GDP has contracted for two consecutive quarters. The situation on the labour market, wages, and corporate earnings is quite the opposite, however. The labour market is in very good shape, wages continue to rise, and corporate earnings are strong. For these reasons, it is rather unlikely that the US economy is already in a recession. But the signs are increasing that this might very well change in the near future. Most leading indicators are already in contraction territory, and initial jobless claims point to a possible change in trend on the labour market. Initial jobless claims have been trending upward for more than four months now. In the past, this has usually been an indicator of an imminent decline in employment and an economic downturn (see chart).

As already illustrated in the last issue of “Our Opinion”, our economic indicator was still slightly above the recession signal. It fell below the mark at the end of July, which is why we can no longer rule out a possible recession.

Equities

As the previous chart shows (highlighted in red), a low point in initial jobless claims often implies a cyclical peak in the equity market. Equity markets have lost value since the beginning of the year, in some cases significantly, but they managed to recover further from their mid-June lows in the month under review. One reason for this is the solid earnings figures of the majority of S&P 500 companies. More than 90% of the companies have now reported their results. Of these, about 75% have presented earnings growth that exceeds estimates (average of the last five years: 77%).

Due to the difficult environment with high inflation, many had expected the figures to be worse.

Analysts likewise expect further earnings growth in the third and fourth quarters. This means there are currently no signs of a recession in terms of corporate earnings (declining earnings in two consecutive quarters). This is likely to have a supportive effect on the equity markets in the short term. We are leaving our Neue Bank traffic light unchanged at yellow/amber (neutral).

Bonds

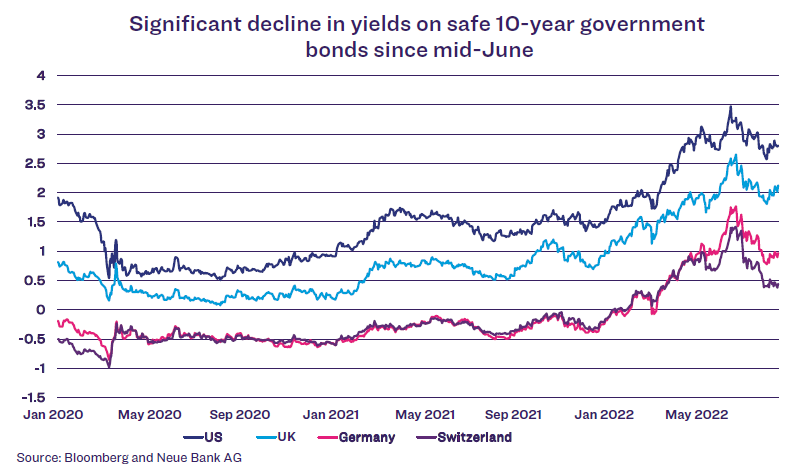

After the strong rise in inflation led to substantial losses on the bond markets in the first half of the year, investors are now increasingly focusing on recession fears again. Demand for safe 10-year government bonds has risen significantly as a result of the gloomier leading economic data. Accordingly, yields have fallen and bond prices have risen.

As long as the labour market does not show any weakness and inflation remains high, the potential for yields to fall further is rather low. Moreover, central banks are still in the process of tightening their monetary policy. We are therefore maintaining our underweight and shorter duration.

Currencies

Investors’ emerging economic fears are also reflected in the currency markets. Safe haven currencies – especially the Swiss franc and the US dollar – are currently in strong demand among investors. For example, the US Dollar Index (measuring the performance of the USD against major currencies) has gained 11.4% since the beginning of the year. Our currency indicator also continues to show a firm USD against all major currencies.

Alternative investments

As fears of recession have risen, some commodity markets have seen significant price losses. The price of oil has fallen 27% since mid-June. An exception is gas, which has risen to new highs for the year.

The price of gas from Europe in particular has veritably exploded.

The Title Transfer Facility (TTF) is a virtual trading point in the Dutch gas network through which natural gas is traded for the Netherlands. The price of a TTF natural gas futures contract is currently at an all-time high of EUR 230. By comparison, the price averaged around EUR 20 from 2005 to the beginning of 2021. This means the price increased more than tenfold in a very short time. The coming winter and Europes high dependence on gas hardly indicate that prices will calm down in the near future.