Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Equities

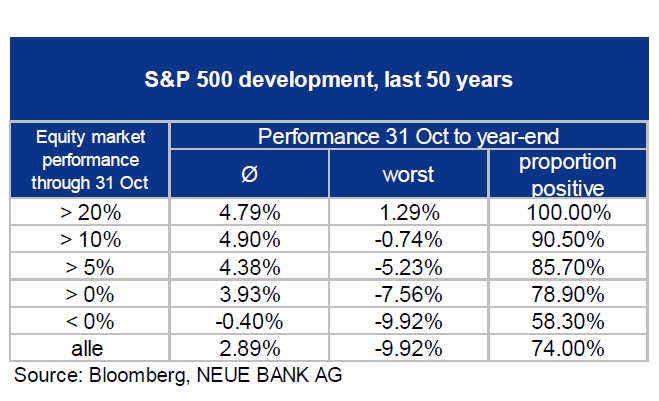

The financial press is full of speculation about whether there will be a year-end rally. This speculation is based on a number of considerations. Some argue that the already high valuation makes further price increases unlikely. Others believe that the strong rise in inflation will lead to a tightening of monetary policy, with a negative impact on share prices. Without denying these two views, we are choosing a completely different approach. We have divided the performance of the equity

market over the first ten months of each year into different growth variables and then examined how prices developed towards the end of the year:

First of all: Statistically speaking, November and December are two of the most positive months on the equity markets. But our analysis shows that this may very well depend on performance through October. In years where the price gains through October already exceeded 20%, year-end performance was also positive without exception. Conversely, the lower the average performance, the higher was the proportion of negative price performance in the last two months of the year. If equity market performance was positive before the beginning of November, the rest of the year was also more successful than the average of all observations. In that light, the research indicates an optimal chance of a year-end rally. The worst precondition for rising share prices at the end of the year is when the first ten months were also a loss. But even then, the proportion of positive year-end performances exceeded 50%. So there would certainly have to be other reasons to completely do without equity investments during the last two months of a year. The NEUE BANK traffic light is light green, which signals a slight overweight in equities.

Economy

Employment in the US is still significantly lower than before the pandemic. Nevertheless, companies are struggling to find suitable workers and are often forced to pay higher wages. Three reasons have been identified in a study. Firstly, seniors over 65 have not returned to the labour market to the same degree as before. Since they belong to the risk group, they apparently are tending to stay home. Secondly, the same phenomenon can be seen among women between 35 and 44. Because of school closures and the lack of childcare options, many are still unable to return to work. And thirdly, temporarily higher unemployment benefits mean that other workers – often including those with lower levels of education – are not yet looking for jobs. It’s an open question of how long it will take until the job market returns to normal. The coming winter with currently higher infection rates does not suggest a rapid easing of the situation.

Currencies

Trust is a valuable asset on the financial markets. What can happen when trust is lost has been evident for quite some time in Turkey. The Turkish lira (TRY) has lost more than 80% against the USD as the reserve currency over the last 10 years. That is more than 15% per year on average. This year again, the loss is already more than 20%, after recent cuts to the key interest rates. Central bank governors have recently been replaced like unsuccessful football coaches. In this way, President Erdogan is at least indirectly exerting pressure on monetary policy. Annual inflation in Turkey is now at about 20%. We do not hold any investments in TRY.

Bonds

To find attractive returns, some investors tend to buy bonds in foreign currencies. When doing so, they often underestimate the currency risk. As an example, we have chosen a Turkish government bond in TRY and one in USD and looked at what the performance in USD would have been over the past years. On the basis of the currency development, the investment in the TRY bond – despite an 11% coupon – would have brought a loss of about 50% over the past 3.5 years. The USD bond, on the other hand, with a significantly lower coupon of 6%, brought gains of more than 30% over the same period. The fluctuations of the USD bond were also significantly lower than those of the TRY bond calculated in USD.

“We therefore advise against investments with currency risk in this asset class.”

This phenomenon is evident not only in emerging market bonds, but also in bonds

with strong credit ratings, albeit less pronounced. Foreign currency risks pay off at

most situationally, but they always ensure higher volatility. This higher risk is not compensated systematically. We therefore advise against investments with currency risk in this asset class. We also avoid emerging market investments in non-investment grade bonds (e.g. Turkey).

Alternative investments

Many commodity prices are currently rising. Investors can profit from these price increases via futures. There would also be the possibility of profiting from rising food prices via agricultural futures (e.g. soybeans, wheat, maize). In some cases, such speculation can raise prices even more (at least temporarily). Since last April, the UBS investable index on agricultural commodities has risen by more than 70%. On ethical grounds, we refrain from this type of investment.