Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Equities

The quick and decisive intervention by central banks, supervisory authorities, and governments saved the banking sector from the worst for now. The financial markets are assuming that Credit Suisse and Silicon Valley Bank are two isolated cases, and they are not currently anticipating a banking crisis. This is also reflected in the lower premiums for credit default swaps at banks in the United States and Europe. This has led to a significant recovery on the equity markets since mid-March. The US S&P 500 index gained more than 5%. Our technical indicators have also improved, which is why the Neue Bank traffic light jumped from bearish (orange) to neutral (yellow/amber) on April 3rd.

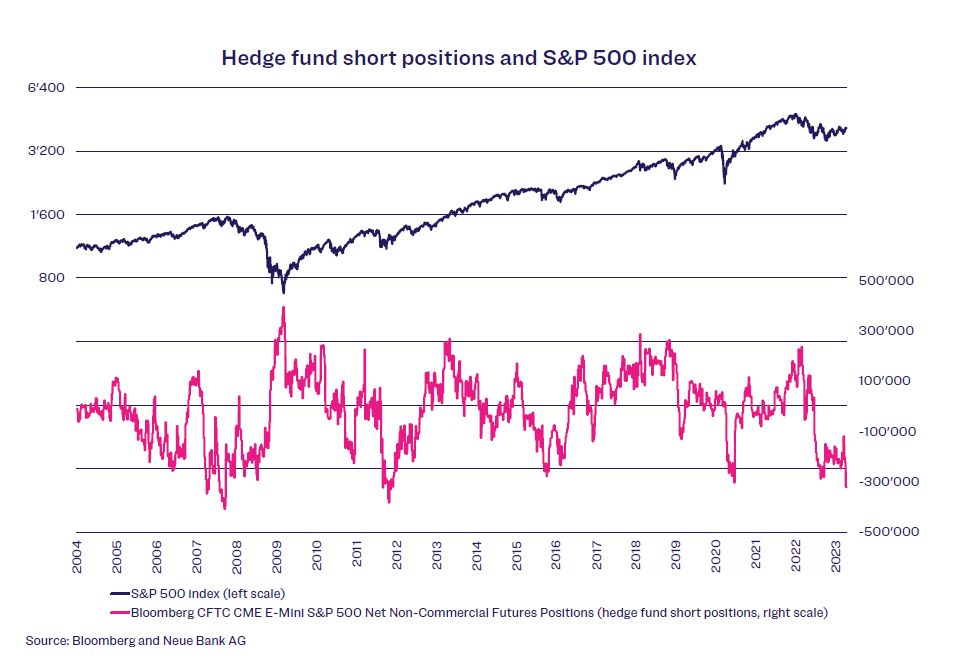

As a result, we have unwound our hedge and rebalanced our equity exposure to neutral. In retrospect, the hedge was not ideal. However, it should be borne in mind that Credit Suisse had to be rescued by the Swiss government – via the takeover by UBS – during this hedging period. If Credit Suisse had not been rescued, this probably would have had devastating consequences for the financial markets, as seen in the 2008 financial crisis. Nevertheless, we still consider the risk of setbacks on the equity markets to be elevated. The reason is that central banks are walking a tightrope with their restrictive monetary policy. The past few weeks have shown how the rapid rise in key rates and the sharp decline in central bank liquidity can lead to an increase in systemic risk. This uncovers misguided developments that have arisen over the past years, requiring them to be resolved in light of changed conditions, which can lead to turmoil on the financial markets. Hedge funds are also expecting more setbacks, as their positioning shows. Their net short positions are now as high as they last were in 2011 and at the beginning of the financial crisis. As we mentioned, we believe that central banks are walking a tightrope, where a small misstep can have grave consequences. We cannot predict the outcome of this demanding tightrope walk, so we continue to be cautious.

Economy

This tightrope walk by the central banks also has implications for the economic trend. On the one hand, central banks have to restore price stability; on the other hand, they should prevent the economy from sliding into a recession. Given the persistently high inflation rates, this continues to be a challenging task. The International Monetary Fund (IMF) also believes the economy is in a risky phase, in which growth remains low by historical standards and financial risks have increased, while inflation has not yet fallen to the target of 2% per year. The IMF is

accordingly lowering its forecast for global economic growth to 2.8%. Meanwhile, even the economists at the US Federal Reserve are predicting a mild recession in the course of 2023. Our economic indicator remains in recession territory.

Bonds

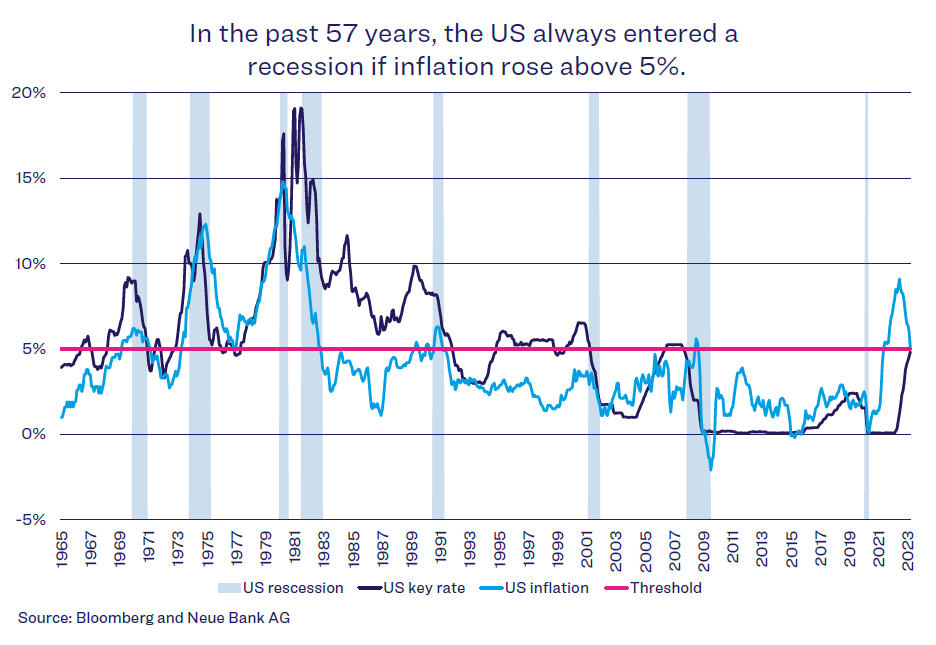

Where there is inflation, interest rates rise. Nothing has changed about this foundation of monetary policy in recent decades. Higher interest rates make loans more expensive, which becomes a burden on individuals, companies, and governments for an extended period of time. This reduces the demand for goods, which causes inflation to subside after a while. The question is, how high must interest rates rise? In the 1980s, the US Federal Reserve responded with massive interest rate hikes, far above the rate of monetary depreciation (see chart).

In the current phase of inflation, we are still a long way from rates of that magnitude, and interest rates are still below inflation (see chart above). To curtail inflation, interest rates probably need to rise less today than in the past. This is because the debt burden of governments and companies has risen strongly in recent years. Given the significantly higher debt than in the past, interest rate hikes have greater leverage. No one can say how high interest rates still have to rise. The mechanisms of national economies are too complex, and interest rate hikes always have a delayed effect. In the past 57 years, however, the US has always entered a recession if inflation rose above 5% (see chart above). Only the future will tell whether central banks will be able to successfully walk the tightrope this time.

Currencies

Now that the banking sector has calmed down, markets are once again riskon. This has also been felt by the US dollar as a safe haven currency, which has dropped significantly against both the Swiss franc and the euro in recent weeks. Based on our currency indicator, we have hedged part of the USD in our CHF mandates since 5 December 2022 and in our EUR mandates since 3 January 2023. Thanks to this tactical hedging, we were able to catch about 5% currency loss against both CHF and EUR. Our key figure continues to signal a weaker USD, which is why we are maintaining these hedges.

Alternative investments

Is gold a crisis currency or not? Opinions are divided. This question does not arise for us at all, however, because we do not hold gold as a permanent strategic position in our portfolios, but rather only as a tactical position – depending on the signal. Since 3 January 2023, we have been holding such a tactical position on the basis of our trading system. The price of gold is mostly strongly correlated with the development of the EUR/USD – weak USD equals strong gold price and vice versa. Because of the current weakness of the dollar, the precious metal gold has gained about 12% since the beginning of the year. The price per ounce is now within reach of the all-time high of USD 2,063 on 6 August 2020. Both the currency signal and the trading system indicate that gold will continue to be strong.