Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Economy

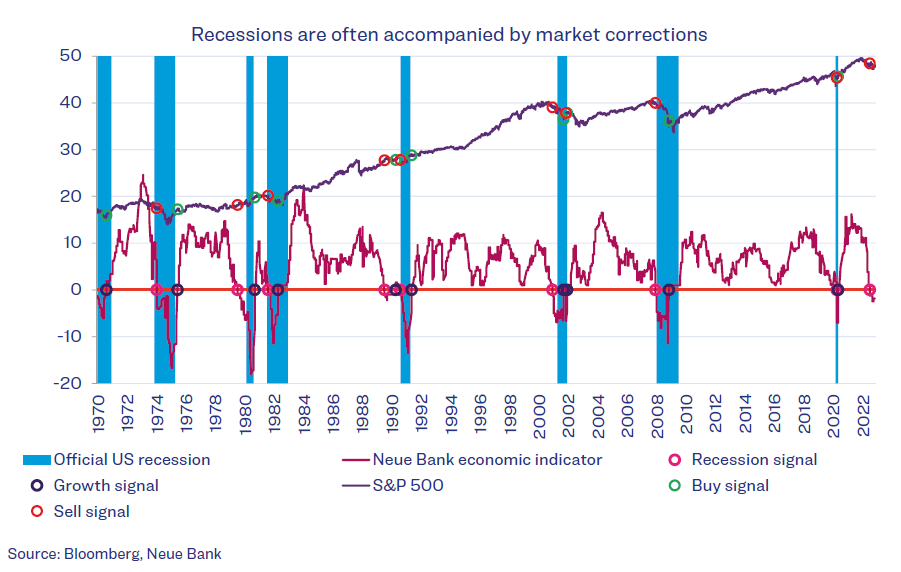

Not always, but often, recessions are correlated with equity corrections. This is why market participants monitor economic developments very closely, trying to identify an economic slump as early as possible. We likewise have developed an indicator to identify an economic downturn at an early stage, given that the official recession data appears only after a delay of several months.

Since 22 July 2022, our indicator has been signalling a recession, which also has an impact on the Neue Bank traffic light. As shown in our chart above, these signals are mostly successful – mainly because the equity markets do not run exactly parallel to the economy, but rather tend to react a bit earlier. The indicator is nevertheless an important component in identifying major market slumps as well.

Equities

But other factors – such as political events, valuations, and sentiment – also have an impact on equity market performance. That is why we have equipped our Neue Bank traffic light with a wide range of indicators. The traffic light is calling for caution (orange), prompting us to hedge part of our equity exposure. The price trend in the reporting month was positive, however. How does that fit together? The traffic light indicates that the risk of setbacks has increased. The reasons are diverse, such as high inflation, disrupted supply chains, high energy prices, fears of a power shortage in Europe, and a strong rise in interest rates.

“More critical have been the problems with the British pension funds. The pension funds had to be rescued by targeted interventions of the Bank of England on the bond market.”

Since the traffic light has been red or orange, quite a few risky situations have indeed occurred. The liquidation of one of the largest crypto exchanges (FTX) need only be mentioned in passing. More critical have been the problems with the British pension funds. The pension funds had to be rescued by targeted interventions of the Bank of England on the bond market. Most recently, however, the publication of US inflation figures – which ended up somewhat below expectations – eclipsed

everything else, and the equity markets reacted euphorically to the news. Nevertheless, inflation is still at 7.7 % per year. Even though it will drop further thanks to the base effect, the 2 % target is still far away. The equity market has of course already priced in a great deal of negativity. But during phases when the traffic light indicates an increased risk, major unexpected events may nevertheless occur that are in no way priced in. One may recall, for instance, the collapse of Lehman Brothers or the near-collapse of the LTCM hedge fund in 1998.

Bonds

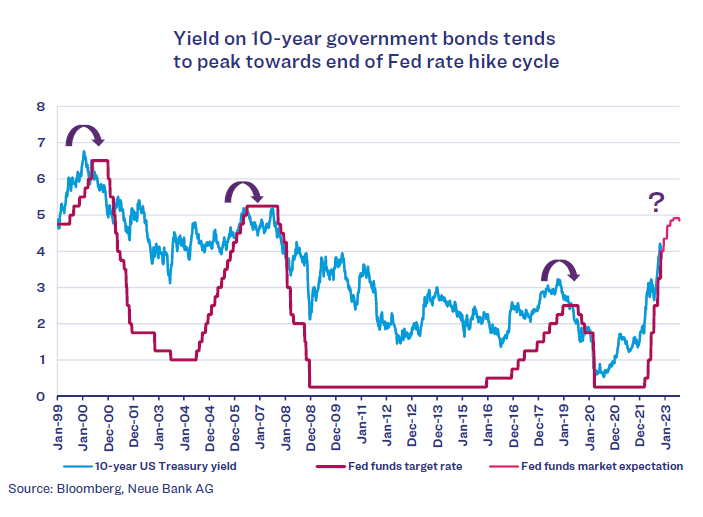

Bonds are looking back at one of their weakest investment years on record. According to research by Bank of America, this has been the worst year for 10-year US Treasuries since 1788. Following that slump, the next few years saw a significant recovery.

At the same time, the rate hike cycle is expected to end by mid-2023. As the chart above shows, long-term government bonds reached their yield peak towards the end of each of these increase phases. We are therefore beginning to extend the duration of certain positions.

Currencies

The Swiss franc (CHF) is considered a safe currency. This makes it all the more important for investors who think in Swiss francs to be careful when making foreign currency investments. For reasons of diversification, we believe including investments in foreign currencies makes sense in principle, but trends may always occur that can have an adverse impact on performance. The beginning of this year saw gains by “commodity currencies” in particular – the currencies of countries whose overall economic accounts include a large share of commodity exports. Examples included the exchange rates of Norway (NOK/CHF), Canada (CAD/CHF), and Australia (AUD/CHF), whose gains were in line with the strong price increases in raw materials (such as natural gas). After the first quarter, however, this price movement changed significantly. The investment community valued the safety factor higher, and the CHF appreciated. This trend became even more pronounced in the second half of the year. Thanks to our currency indicator, we hedged our positions in those currencies in our CHF mandates in the second half of the year.

Alternative investments

Last month, we noted that cat bond investments had come under pressure after Hurricane Ian hit Florida. The feared flood damage of about USD 60 billion did not materialise. Official estimates now assume losses in the range of USD 3.6 to 5.3 billion. As already suspected, the price setbacks may have represented a good entry opportunity. The fund we selected in this segment even assumes that none of its cat bonds will default, and it stocked up the flood damage sector again somewhat. Prices have not yet fully recovered, which is why buying still appears attractive.