Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Currencies

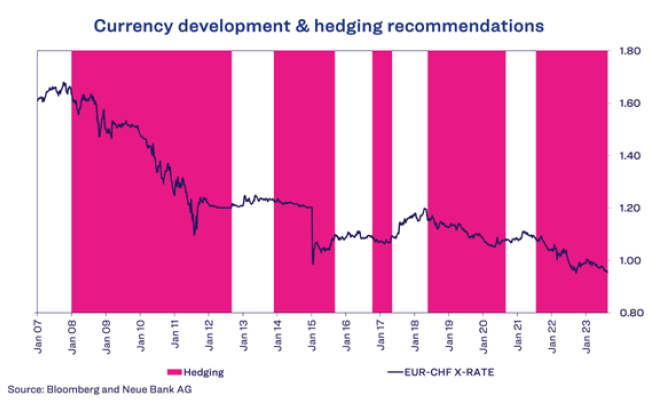

Since the financial crisis, the EUR/CHF exchange rate has moved in only one direction, namely down. In the autumn of 2007, the exchange rate was still around 1.68 Swiss francs per euro. The current EUR/CHF rate is at 0.955. This means the euro has lost about 43% of its value against the Swiss franc. The same trend can be seen against all other currencies. There is currently not a single currency that has gained against the Swiss franc since the financial crisis. Among those that have lost the least is the USD at “only” 25%. A Turkish lira (TRY) is practically worthless, having dropped 97% against the CHF. Several factors explain this phenomenon. Switzerland has favourable economic conditions, high productivity, and low inflation – alongside political stability and low public debt. Just recently, the rating agency S&P once again affirmed Switzerland’s creditworthiness with its top rating of AAA, praising the country’s “strong economic resilience”. Thanks to these circumstances, the Swiss franc is considered a safe haven. On the other hand, there have been repeated warnings that the strong currency could also harm Switzerland, since it would make domestically manufactured products more expensive, which could become a problem for the heavily export-oriented economy.

This has not proven to be true so far, however. On the contrary: in the current environment of high inflation, Switzerland is benefiting particularly from the strong franc. The economy is able to import at cheaper prices, resulting in lower inflation and lower cost increases. Inflation in Switzerland is currently a low 1.6%, compared with 5.3% in the Eurozone. Given this context, we continue to see little headwind for the Swiss franc in future. Our currency indicator likewise confirms this picture. Since July 2021, we have been hedging the EUR in our CHF mandates. As the following chart shows, there have been five phases since the financial crisis during which we have hedged the euro, allowing us to cushion its drop in value.

Economy

The current economic data continues to point to a weakening of the economy. In the United States, the Purchasing Managers’ Index (PMI) for manufacturing is still below the growth threshold of 50, while the services sector is still slightly above. The PMI results from the Eurozone paint a clearer picture. There, both manufacturing and services are below the critical threshold, pointing to a possible recession. The economic indicators included in the Neue Bank traffic light have recovered, but they are still slightly inside the recession range.

Equities

Have we almost reached peak interest rates in the United States? Since March 2022, the US Federal Reserve (Fed) has raised the key rate by 525 basis points, from 0.25% to 5.5%. Given the current economic concerns and the easing of the labour market, interest rate markets are pricing in no further hikes from November on. If the Fed follows market expectations and stops tightening monetary policy, this could give the equity market a further boost. Over the past 45 years, the US equity market has gained an average of 22.5% in the two years following the last rate hike. The current cycle can best be compared with the phase between the beginning of 2004 and the summer of 2006, when the Fed raised key rates at nearly the same pace. The context at the time was likewise an overheated national economy and rising inflation data. After the end of rate hikes in June 2006, the S&P 500 rose by another 20% until the outbreak of the financial crisis. During that phase, the Fed had raised interest rates too much, however, which notoriously led to a hard landing and the financial crisis. No one can answer whether the Fed has already overshot the mark. Right now, the market is assuming a soft landing with moderate economic growth. If the development is similar to the past, equity prices can be expected to continue to rise. The Neue Bank traffic light is still neutral (amber/yellow), but it might even switch to slightly bullish (light green) in September if economic data is better than expected. For now, however, we are maintaining our neutral equity weighting.

Bonds

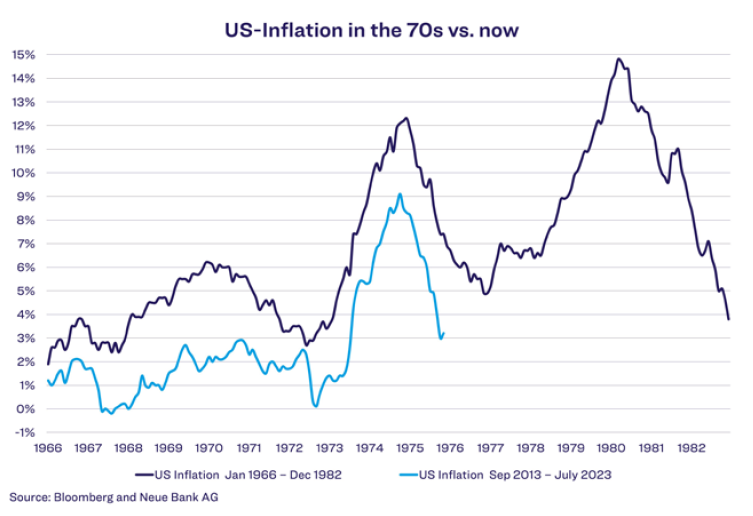

Is Fed Chair Jerome Powell afraid of the following chart?

The chart shows the development of US inflation from January 1966 to December 1982 compared with September 2013 to July 2023. The trend is very similar, except that inflation peaked somewhat higher in the 1970s than during the current phase. In March 1980, the Fed lowered the key rate from 20% to 11.5%. But this was followed by a second wave of inflation, which peaked at just under 15%. It is precisely such a renewed surge that Jerome Powell is concerned about, which is why he has not yet declared victory over inflation. At the central bank symposium in Jackson Hole, the Fed Chair said that while the Fed had come a long way in its fight against inflation, the 2% target had not yet been reached. This is why he is determined to raise interest rates further if necessary and to keep them at a restrictive level until there is certainty that inflation will move towards the target on a sustained basis. Jerome Powell is accordingly leaving all options open, and investors may have to brace themselves for an extended period of higher

interest rates.

Alternative investments

Many investors believe that including gold in a portfolio is essential to protect against inflation and crises. Last year, however, when all asset classes corrected, this did not turn out to be true; instead, gold correlated with both the equity and bond markets and did not contribute the desired diversification to portfolios. From January to October 2022 – when the US equity market hit its lowest point of the year – gold lost nearly 10%. Even taking a long-term view, the performance of equities is significantly better than that of gold, even though their fluctuations (volatility) are roughly the same magnitude. For this reason, we do not hold gold in our portfolios on a permanent basis, but rather use it only depending on the signal. We are not currently holding gold, but instead are invested in listed private equity.