Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Economy

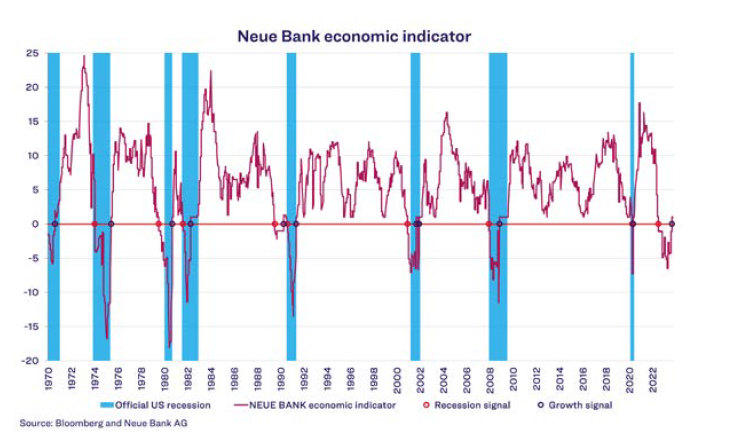

The US economy grew by an annualised 4.9% from July to September, more than doubling the growth rate of the previous quarter. This is the strongest increase in nearly two years. So far, there has been no sign whatsoever of the recession in the United States expected by economists at the beginning of the year. Starting in July 2022, our economic indicator likewise pointed to a US recession. As the following chart shows, since 1970 there had always been a recession when the indicator fell

below minus 5 points.

Since the beginning of September 2023, the economic indicator has even been above the red line again, indicating growth. The signal turned out to be false, along with the models of many other market experts. There is now even increasing talk of a “no-landing” scenario, which assumes that economic growth will continue to boom despite the already significantly increased interest rates, and that inflation will remain above the 2% target of the US Federal Reserve (Fed). This scenario is supported by the strong economic data coming from manufacturing and consumers. This could become a problem for the Fed, however, given that it has been trying to achieve a soft landing with its interest rate hikes so far. In a soft landing, the growth rate weakens (but does not become negative), with the aim of bringing inflation below the target level. If the Fed believes its plan is in danger, this could result in further interest rate hikes, which in turn increases the risk of a hard landing, i.e. a recession. The market consensus for the US continues to assume a soft landing. The situation is quite different in the Eurozone, where the economic data has continued to become more negative and in some cases is clearly in recession territory. Due to the worsening data, the European Central Bank (ECB) decided at its meeting on 26 October 2023 to pause interest rate hikes. Many market participants believe that this step is too late, and that a hard landing of the European economy at the beginning of 2024 can no longer be avoided.

Equities

Should a no-landing scenario occur, this will likely weigh on the equity markets, given that further interest rate hikes would then be expected. Higher interest rates worsen the financing conditions for companies, which has a negative impact on their balance sheets. The first few companies, including Alphabet, already reported disappointing quarterly figures. The equity markets then continued their correction that had already been triggered by the escalation in the Middle East. The Neue Bank traffic light is still slightly bullish, but it could soon switch to neutral if the correction continues or even worsens.

Bonds

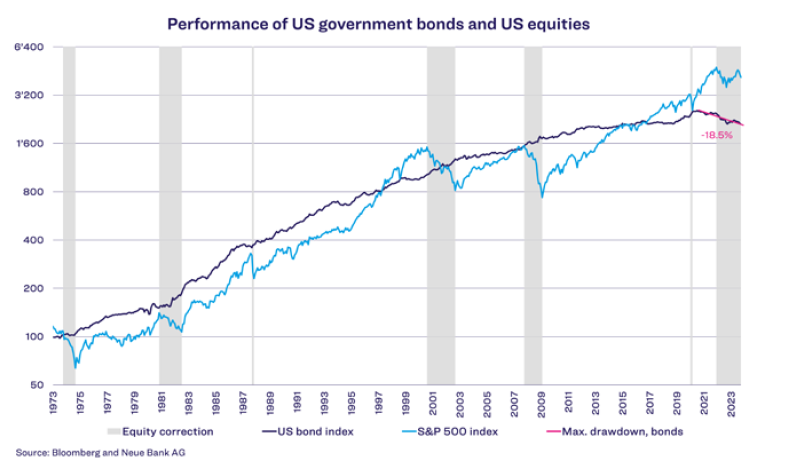

Yields on the bond markets continued their upward trend. On 23 October 2023, the yield on 10-year US Treasuries rose to just over 5%, the highest since the financial crisis. The yield is now just below that mark. This development was triggered by the worries that the no-landing scenario described above might occur, which would mean that the fight against inflation is not progressing as quickly as the Fed would like. Market participants now fear further interest rate hikes, which has led to an increase in the correlation between equities and bonds. This means that bonds offer less protection when equities correct, given that they also lose value. The diversification effect in the portfolio is diminished, because bonds add to risk instead of reducing it. The chart on the next page illustrates this problem.

During equity corrections in the more distant past, government bonds were always able to increase in value, reducing the portfolio risk, because they were able to cushion equity losses. This effect is not currently working, given that both equities and bonds are losing value. Historically, bonds are experiencing the strongest setback in their history in terms of both value (-18.5%) and duration (nearly 3 years already). This has led to a disappointing performance of mixed mandates with higher bond exposure since 2022. Only once the interest rate situation calms down will bonds be able to gain again.

Currencies

Last month, a currency signal was triggered for the EUR/USD. Our trend indicator now advises to no longer hedge USD positions in EUR portfolios. Consequently, we have removed the currency hedge in our EUR mandates. The signal is in line with the currently exacerbated geopolitical situation, in which especially currencies like the US dollar and the Swiss franc are serving as a safe haven.

Alternative investments

The real estate crisis in China continues to worsen. For the highly indebted Chinese real estate group Country Garden, the grace period for an interest payment on a dollar bond in the amount of USD 15 million ended on Tuesday, 17 October 2023. The group announced that it is unable to service the foreign debt. According to the international Credit Derivatives Determinations Committee, this amounts to a default. The group’s total corporate debt amounts to USD 200 billion, of which USD 17 billion is foreign debt. If Country Garden does in fact fail, this could have far-reaching consequences for the entire Chinese real estate sector. The real estate market generates about 20% of China’s GDP. An expansion of the crisis would accordingly have devastating consequences for the Chinese economy. This would hardly affect economic output in industrialised countries, however, given that most of the debt is domestic and was not securitised and sold worldwide as safe bonds, as had been the case in the 2008 financial crisis.