Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Bonds

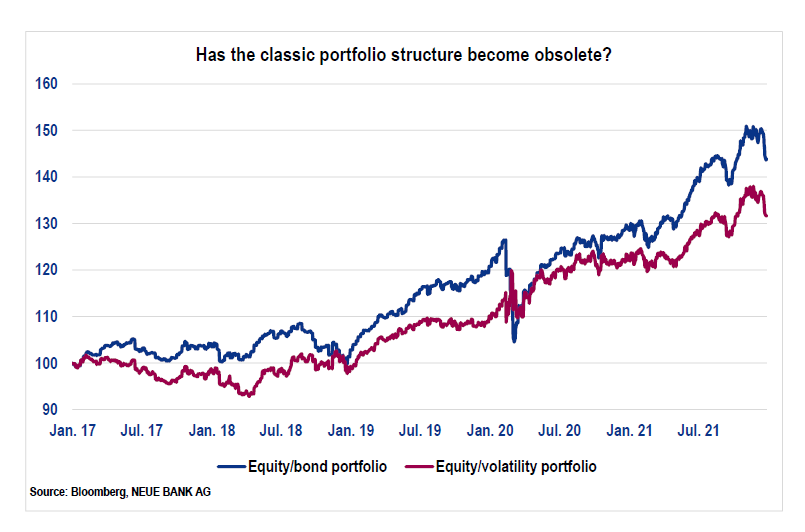

For decades, bonds were considered the ideal diversification for equity investments. But now that yields on AAA bonds have fallen below zero, more and more investors are calling this status into question. An investment where a loss is a foregone conclusion does indeed not appear attractive. This is why the financial industry is always looking for alternatives. Some add corporate bonds with lower credit ratings to the mix, but they have the disadvantage that they react significantly more cyclically during crises – with an increasing correlation to equity investments – which has a negative impact on portfolio risk. Instead of cushioning the losses, investors often lose even more money with these bonds during recessions. Others add foreign currency bonds to the mix. But since currencies have higher volatility than safe bonds, this also leads to an undesirable increase in risk. Moreover, studies show that this higher risk does not systematically lead to higher returns.

An alternative may be to resort to volatility products. Although they likewise do not generate regular returns, they can significantly reduce portfolio fluctuations thanks to their negative correlation with equities. In the chart above, we compare a portfolio with 50% equities and 50% bonds to a portfolio with equities and a volatility product. Thanks to the good diversification characteristics, we were able to consider a ratio of two-thirds equities to one-third volatility, and even then, the maximum setback during this period was lower for the equity/volatility portfolio than for the traditional portfolio (-12.31% compared to ‑17.40%). Thanks to the higher share of equities, the annual return of the equity/volatility portfolio was 1% higher, at about 8%. Especially after yields on 10-year bonds reached their low point in August 2019, performance of the equity/bond portfolio was no longer able to keep up. Does this mean the classic portfolio structure has become obsolete? We would not go that far. However, an addition of alternatives like these can certainly be considered. Our advisers will be happy to help you with your product selection.

Economy

Inflation has recently risen to unusual highs. While the US core rate (excluding food and energy) fluctuated around 2% for two decades, it reached 5.45% at the beginning of the year. Including food and energy prices – which are subject to strong fluctuations – the rate was even 7%. There is still some dispute as to whether this increase is mainly due to supposedly temporary supply bottlenecks or whether, as a result of expansionary monetary and fiscal policy, a dangerous acceleration is taking place that must be combated with significant interest rate hikes. This question is currently occupying the financial markets. Our economic indicator suggests that we are in the final phase of an upswing, but that a recession is not yet imminent.

Equities

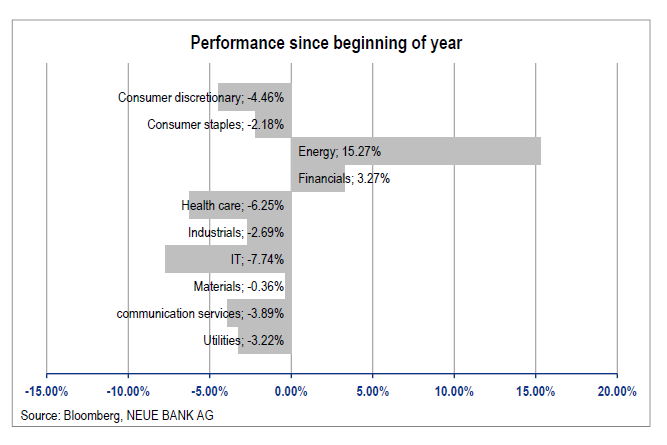

Due to uncertainties regarding possible interest rate increases, sector rotations occurred on the equity markets.

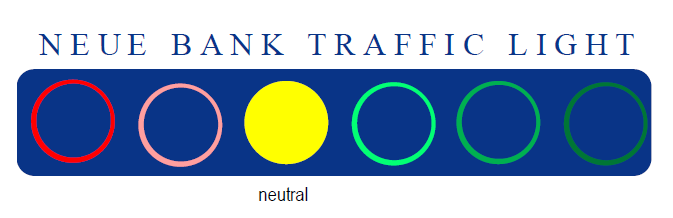

The technology and health care sectors, which had previously been performing well, suffered setbacks. In the event of rising interest rates, the expected earnings would have to be discounted at a higher rate, resulting in a lower present value. Conversely, financials are benefiting from rising interest rates and the energy sector from rising oil prices. Our equity selection significantly outperformed last year after a mixed start; we are again lagging the market at the beginning of the year. But again, we will not completely change our equity selection overnight, and we will instead stick to our proven rebalancing cycles. Our traffic light is still at neutral.

Currencies

Currencies can have a decisive influence on investment performance – such as the JPY, which often tends to weaken when equity markets rise. For portfolios with CHF as their reference currency, for example, we have hedged the Japanese currency since mid-December 2019. Since then, the Nikkei has gained about 17% in local currency. Due to the exchange rate development, however, the gain measured in CHF is less than 5%. This means the currency has had a greater impact on performance than the development of the equity market. Active currency management can therefore make a valuable contribution to performance. Based on our indicators, we continue to hedge the JPY.

Alternative investments

Exactly one year ago, we wrote about commodity investments in this space. We drew attention to a long-term trend reversal formation of the UBS Bloomberg CM Commodity Index. The index was then on the threshold of a breakout at USD 1,000. We are meanwhile just below the price target at that time of USD 1,350. Should one still remain invested now? The trend is intact. A stock market rule says, “The trend is your friend”, which means to stick with it as long as the trend does not turn around.