Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Economy

As Warren Buffett once said, “You don’t find out who’s been swimming naked until the tide goes out.” Applied to today’s situation, this means: When the central banks’ expansionary monetary policy is scaled back, you can see who’s financed well and hasn’t taken on too much risk. Silicon Valley Bank (SVB) – the 16th largest bank in the United States – has been swimming naked. It made the mistake of investing deposits in long-term bonds. When customers withdrew their money, the bank was forced to sell the bonds. Because of the strong increase in yields, the bank was hit by price losses. This caused distress for SVB, eventually leading to its insolvency. Credit Suisse (CS) also struggled with outflows after repeatedly delivering negative headlines in recent years. To prevent a bank run, the Swiss Federal Council brokered a takeover of CS by UBS. The takeover was not free of criticism, but it has calmed the financial markets for now. Already in 2008, the global financial crisis triggered a worldwide recession involving the rescue of several banks – while others, such as Lehman Brothers, one of the largest US investment banks, went bankrupt. Is this a déjà vu? The problems were different in 2008. Mortgage loans had been securitised and rated as safe by rating agencies. This went well – until the collateral (real estate) lost value. Many banks had trusted the agencies when rating these less transparent products and ended up losing money on their investments. This time, the problem is apparently more about mismanagement of the banks’ own balance sheets. The central banks reacted quickly, providing liquidity to banks.

Bonds

Central banks are caught between a rock and a hard place, however. They are trying to fight high inflation with a restrictive monetary policy – but this can also worsen the financial stability of some banks. The ECB has already adjusted its wording somewhat, moving towards a less constraining policy. The Fed may soon do the same. Yields on safe government bonds declined during the reporting month, in contrast to bank bonds.

Equities

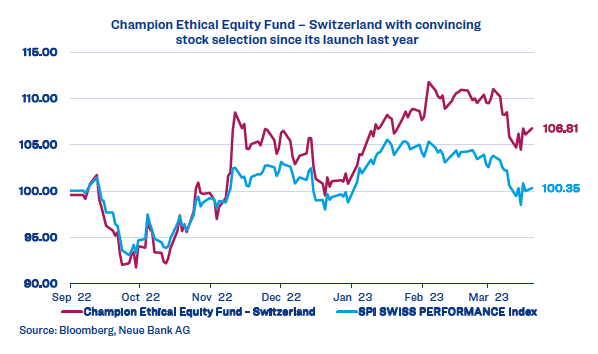

Banks also came under significant pressure on the equity markets. Based on our quantitative analysis, we had underweighted banks. Already for about a year, we had been recommending Credit Suisse shares as a sell (and before that, our assessment had already been underweight). Thanks in part to this and similar advice, the Champion Ethical Equity Fund – Switzerland, for which we serve as investment advisors, significantly outperformed the overall market both in the reporting year and since its launch.

In mid-month, the Neue Bank traffic light switched back to bearish (orange), which is why we hedged part of our equity exposure. US regional banks continue to generate some uncertainty. Because of relaxed regulations in the United States, it cannot be ruled out that other banks have struck a poor balance in their asset-liability management. On the day after the CS takeover, for example, the San Francisco regional bank First Republic Bank lost nearly 50% of its value, bringing its year-to-date loss to about 90%. This shows that the market does not fully trust all credit institutions.

Currencies

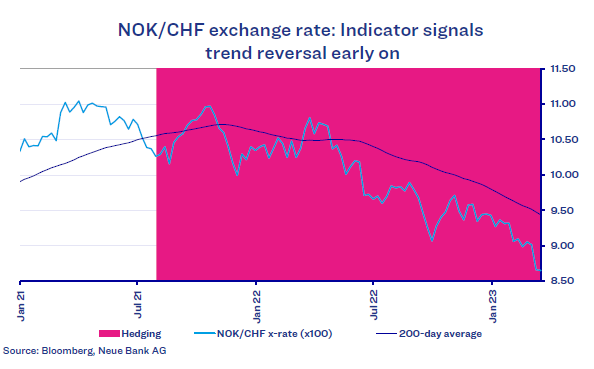

Forecasting foreign currencies correctly is an especially difficult undertaking. This can be seen using the NOK/CHF exchange rate as an example. Even before Russia’s attack on Ukraine, crude oil and gas prices were rising significantly. After Europe gradually shifted its energy sources to other suppliers due to the Russian aggression (away from Russia, towards Norway and others), energy costs continued to rise. Quite a few observers would have expected the Norwegian krone (NOK) to rise during such a phase.

But looking at the exchange rate development during this period (see chart), the NOK/CHF exchange rate depreciated precisely during that phase. Our currency indicator already indicated a trend reversal in the summer of 2021 (hedging signal), which subsequently did indeed occur. To obtain these signals, we limit ourselves to technical indicators and do without geopolitical analyses. As the case of this currency pair shows, hedging the NOK in our CHF portfolios significantly mitigated the currency loss.

Alternative investments

At the beginning of the year, our trading system for alternative satellite investments generated a buy signal for gold. The ounce was trading at USD 1823.00 at the time. On 20 March 2023, the price even rose briefly above USD 2000.00. The precious metal benefited from the fear of a possible banking crisis. In this way, gold fulfilled exactly the purpose of alternative investments, namely not to lose value in parallel with the markets, but rather to offer a negative correlation and positive diversification effect during these phases.