Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Equities

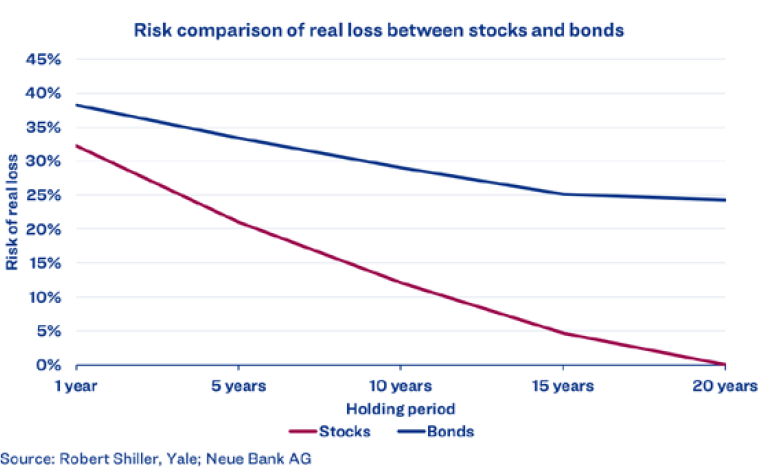

Can stocks have a lower risk than bonds? In the financial world, risk is usually equated with volatility. According to this measure, it is clear that equities have a higher risk than fixed-income investments. As an alternative measure of risk, however, the probability of a loss that may occur after a certain holding period could also be used.

We have tested this measure for the US equity market over the last approximately 150 years. After a holding period of 20 years, the probability is close to 0 % that a broadly diversified investment in equities will result in a loss, even taking inflation into account. The longer the investment horizon, the lower the risk of having lower assets at the end of the term than at the beginning. A study published last year recommends that US investors invest less in the widespread 60/40 portfolios (60 % stocks and 40 % bonds) and more in a broadly diversified equity portfolio.

Bonds

In our part of the world, however, it is still customary to also ask the client about their ability and willingness to take risks. This is a good thing, because nothing is more disastrous than changing your strategy at the wrong time. All too often, investors throw everything overboard after a major setback on the equity markets, reducing their proportion of volatile stocks. The chart above shows that bond investments were also susceptible to real losses – even after twenty years. This is because inflation has often been higher than bond yields. Some investors might jump to the conclusion that they should avoid bonds altogether. However, inflation losses are of course also incurred on cash and account balances. In the past, these losses have been significantly higher than with bond investments. If the fluctuations of equity investments are too high, it of course makes sense to add bonds to the portfolio, reducing portfolio volatility.

Economy

Growth expectations for 2024 are low, and a recession still cannot be

ruled out. Important elections are coming up this year (especially in the

United States), and geopolitical tensions continue to dominate the daily

headlines. The consequences of these events could of course have an

impact on economic development. It will also be interesting to see how

monetary policy develops. Several interest rate cuts have already been priced in by the market. Deglobalisation is progressing, which is likely to lead to structurally higher inflation, after we have benefited from very stable prices over the last few decades thanks to the global division of labour. Although our economic indicator does not point to an immediate recession, it remains close to critical levels.

Currencies

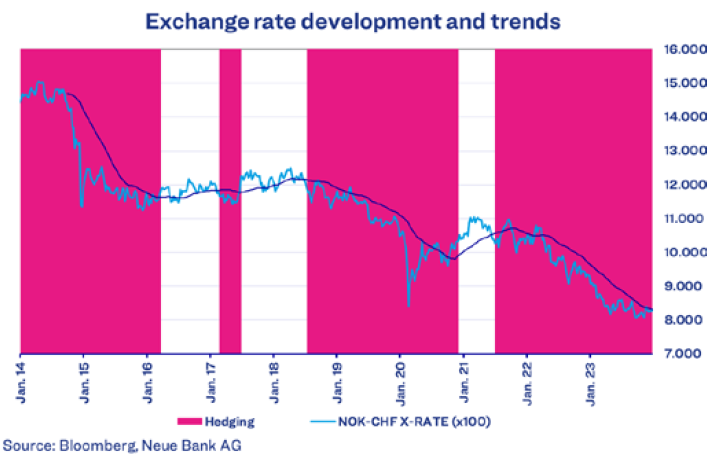

Both Norway and Switzerland have the reputation of being extremely stable European economies outside the Eurozone. Nevertheless, the exchange rate between NOK and CHF has tended to move in only one direction over the last 10 years.

While the NOK/CHF exchange rate (x100) was still at around 15.00 10 years ago, it is now just over 8.00. Anyone who added shares in Norwegian companies to their portfolio during that period would have been susceptible to significant currency losses. During those phases, our currency trend indicator called for foreign currency risk to be hedged. Investors from the CHF currency area in particular should take a close look at foreign currency risks, given that their home currency has always been very strong in the past. We also continue to hedge NOK equities in our CHF reference currency portfolios.

Alternative investments

In economics – in contrast to chemistry – there are only four precious metals. Alongside gold, silver, and platinum, palladium is also traded as a precious metal. The greatest demand for palladium comes from the automotive industry, where the metal is used to manufacture catalytic converters. Russia is one of the largest producers of palladium. This is also one of the reasons why its price rose to over USD 3,000 per ounce in the run-up to the Russian invasion of Ukraine. The price has since fallen below USD 1,000. We will refrain from speculating as to when this price slump will bottom out. Our trend indicator continues to advise against investing, in line with the stock market adage “never catch a falling knife”.