Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Equities

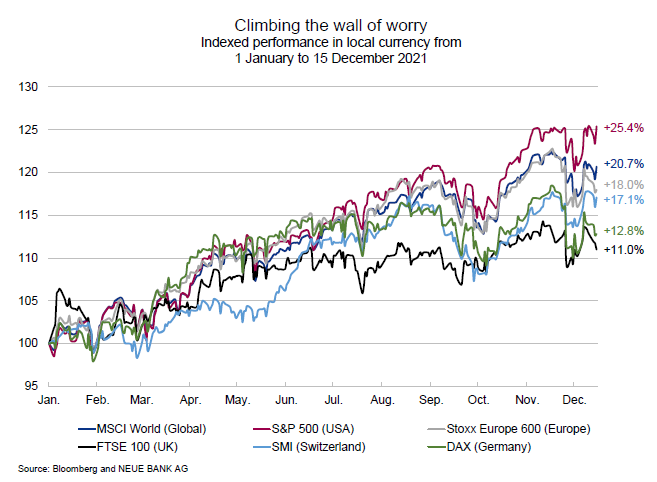

Another eventful year is coming to an end. Delta, Omicron, record government debt, rising inflation, negative real interest rates, economic worries, and high equity valuations are just a few of the fears that have accompanied investors this year. Despite all these risks, investors – who did not allow themselves to be rattled – were able to achieve considerable returns through equity investments. The most important market indices reached new all-time highs and are clearly in the black:

This phenomenon is called “climbing the wall of worry”. With each further rise in the equity markets, the pain and fears of investors who are not yet invested increase. No one wants to miss out on the rally, and little by little investors enter the market despite their scepticism. A wall of worry can last a very long time and often only ends when the sentiment becomes very euphoric. In our view, the wall of worry still has potential in the coming year. Despite possible monetary tightening, expansionary central bank policies continue to be a support for the markets. Moreover, the persistently negative level of real interest rates should mean that the TINA argument (“there is no alternative”) will continue to hold, and equities will remain the preferred asset class. Due to the increased volatility in the reporting month, the NEUE BANK traffic light has fallen from green to amber, which has caused us to reduce our equity exposure to neutral.

Economy

At the beginning of the year, concerns about economic development surfaced due to the Delta variant of the coronavirus. In retrospect, however, these concerns were unfounded, and the recovery of the global economy continued with an above-average growth rate. We are currently in the same situation again with the Omicron variant. With each wave of the pandemic, however, the negative impact on the economy has diminished, and a weak quarter has been followed by a strong one. The economy has learned to cope with the virus. We therefore expect strong economic growth in 2022 as well, given that there is still a gap to precrisis levels in some areas and the catchup effects are likely to continue.

Bonds

Due to the economic recovery and rising inflation, yields rose this year – in some cases significantly – which consequently led to lower bond prices. Investment grade bonds have hardly made any money this year. The Bloomberg Global Aggregate Bond Index, for example, has lost about 2% in currency-hedged terms against the CHF. In the US, inflation rose to 6.8% in November – the highest level since the early 1980s. Until now, central bankers believed that inflation was only temporary. But the price pressure is more persistent than expected. In light of this, central banks are coming under increasing pressure to adjust their ultra-expansionary monetary policy.

The US Federal Reserve will reduce its bond purchases more quickly than planned, implementing initial interest rate hikes as early as next year. In the Eurozone (4.9%) and Switzerland (1.5%), price pressure is not yet quite as high, which is why the ECB and SNB will probably not be forced to start raising interest rates in 2022. If inflation proves to be persistent, a difficult environment in this asset class should also be expected next year.

Alternative investments

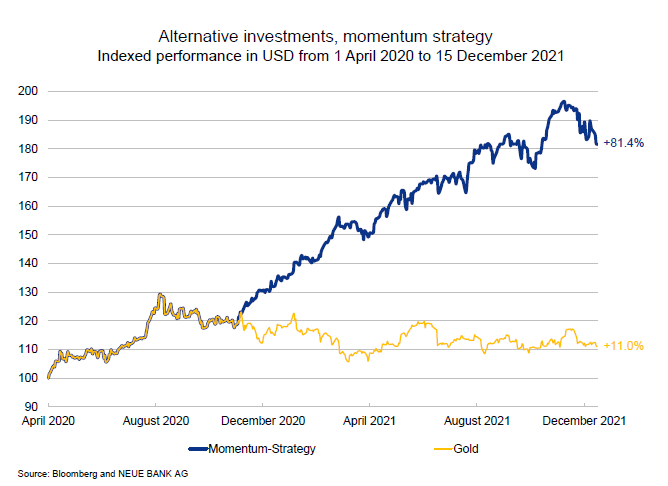

The story that gold could serve well as an inflation hedge in the portfolio has not proven to be true this year, despite strongly rising inflation rates. On the contrary, the yellow precious metal has fallen about 6% (in USD) since the beginning of the year. In our asset management mandates, gold is not a fixed component of the asset allocation, but can be included in the portfolio only as a tactical position as part of our momentum strategy. This was most recently the case from the end of March 2020 until the end of September 2020. The position was then swapped for a broadly diversified commodity ETF. The next signal came at the beginning of April 2021, when we switched the commodity ETF into a listed private equity ETF.

This dynamic approach has allowed us to generate significant outperformance for our clients compared with a pure gold position (see chart).

Currencies

Normally, the Swiss franc tends to weaken when the markets switch to “risk on” mode. This year has been very different: The CHF has appreciated against all major currencies – except the USD. The high current account surplus, the low level of government debt, and the still relatively low interest rate differential make the CHF attractive in both good and bad times. This is likely to remain the case for now. Our trend indicators also reflect this picture and advise hedging foreign currencies against the CHF, with the exception of the USD.