Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Equities

Persistently high inflation and the associated response of central banks in the form of interest rate hikes continue to be the dominant themes on the financial markets. This led to further – and in some cases significant – price losses on the equity markets during the reporting month.

On the US equity market S&P 500, the bear has started to dance.

The index is down 23.5% since the high at the beginning of January. This is a bear market by definition (price loss greater than 20%). A look at the history of bear markets shows that a quick V-shaped recovery, as in the 2020 coronavirus crisis, is the exception rather than the rule. Financial services provider Susquehanna International has analysed all 12 bear markets since 1945 and found that when entering a bear market, the S&P 500 falls another 14% on average and takes 103 trading days before bottoming out. Adapting the historical pattern to the current situation, this would mean that the S&P 500 would bottom out in November at about 3250 points. No one knows whether this will happen, but investors should prepare for continued volatility on the markets due to the difficult situation with inflation, war, interest rate hikes, and cooling of the economy. The Neue Bank traffic light has likewise reacted, dropping from slightly bullish to neutral. Consequently, we have reduced our risk assets from a slight overweight to neutral.

Bonds

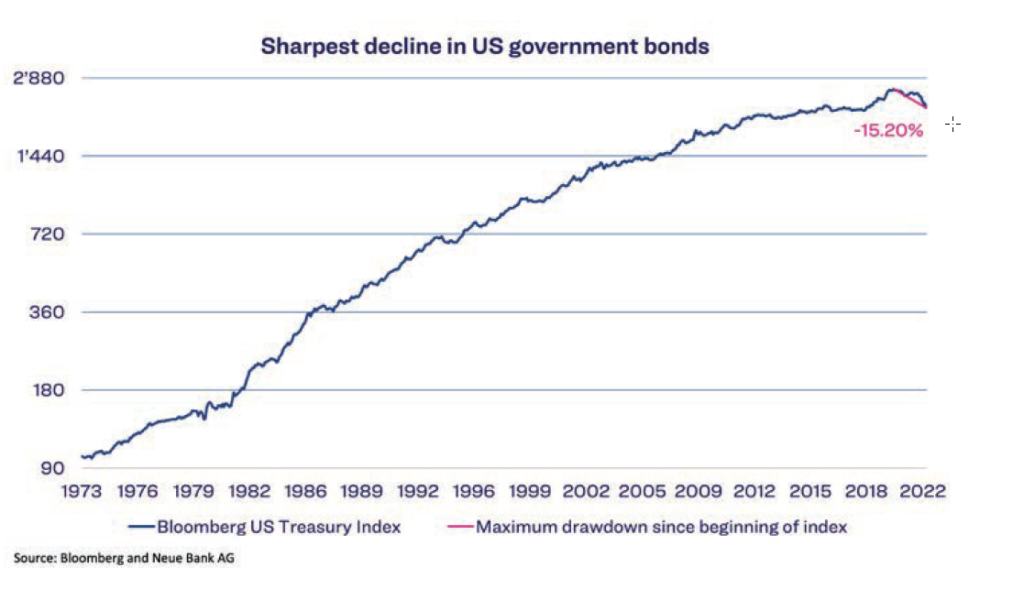

There is no generally accepted definition of a bear market for bonds, but with a decline of -15.20% in the index of safe US government bonds (see chart on next page), the bear appears to have taken the reins in this asset class as well. Moreover, this is the biggest setback since the beginning of this index. The counterpart for Eurozone government bonds has even fallen 18.1%, almost the same decline as the European equity market.

A nearly equally strong correction of equities and government bonds in uncertain times is unusual; this is due to the extremely low interest rate environment. In the past, when interest rates were higher, the higher coupons served as a buffer when yields rose. Now, with negative interest rates, this buffer is missing. If yields rise sharply – as is currently the case – the price of bonds also falls more sharply. As an example: A 10-year German government bond with a coupon of 0% had a yield of likewise 0% at a price of 100 at the beginning of March. By mid-June, the yield had risen to nearly 1.7%. In order for the zero-coupon bond to generate a yield in line with the market, the price fell to about 84, representing a price loss of -16%. This indicates that investors must temporarily expect strong fluctuations in the value of bonds as well. But this does not mean that bonds are losing their function in a diversified portfolio.

Especially in the current environment, however, it is all the more important to pay attention to quality.

For that reason, we are focusing our portfolios on safe government and corporate bonds with high credit ratings.

Economy

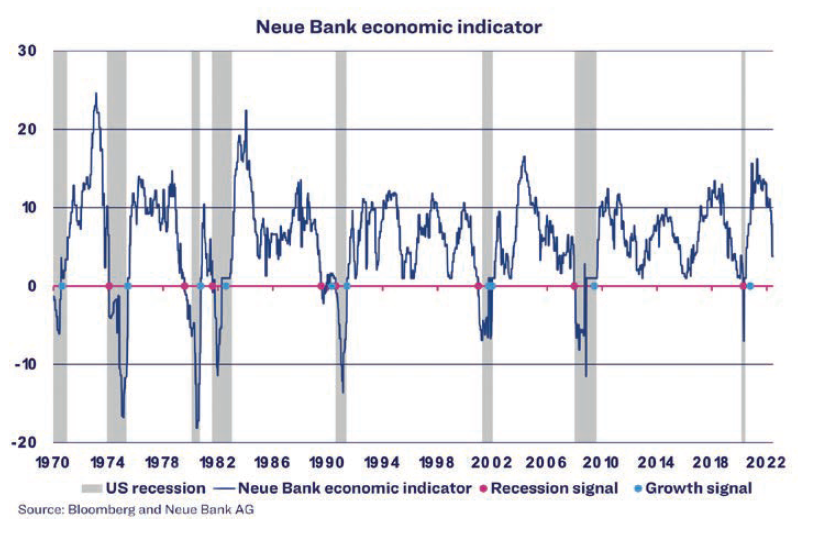

US economic data in the reporting month shows that high inflation is increasingly interfering with growth in the US economy. For example, US retail sales have surprisingly shrunk. Sentiment in the US housing market also became gloomier in June, with the interest rate on 30-year fixed mortgages doubling from 3% to 6%. Activity indicators in the manufacturing sector have also been a negative surprise. The Philadelphia Fed and New York Empire indices, for example, are both in contraction territory. Leading indicators have also fallen, signalling a significant slowdown of growth. Our economic indicator is also signalling a slowdown, but no recession yet.

Currencies

The bear is also dancing on the currency market. The Japanese yen has lost almost 16% of its value against the USD since the beginning of the year, falling to its lowest level since 1998. The JPY is even at an all-time low against the Swiss franc (-11% since the beginning of the year). The extremely weak yen is due to the monetary policy of the Bank of Japan. Japans central bank has so far resisted the global trend towards monetary tightening and is steadfastly sticking to its loose policy with a negative key interest rate and yield curve control. We have been hedging our JPY positions in our CHF and USD mandates for quite some time and

continue to do so.

Alternative investments

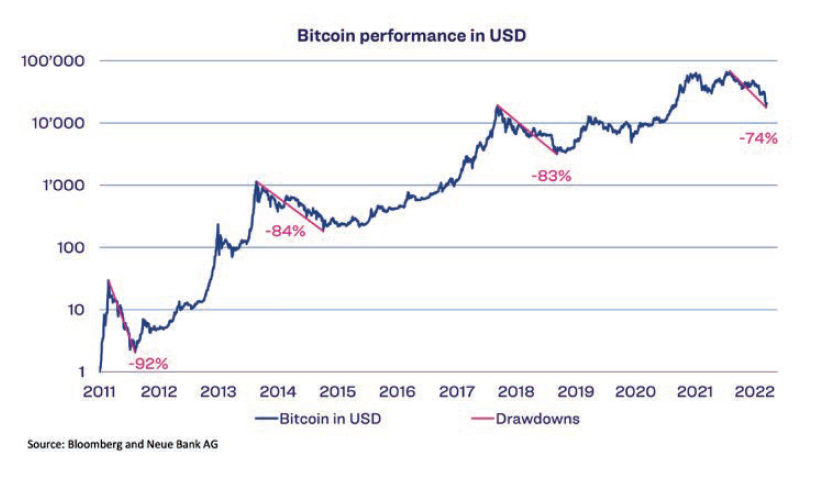

In the crypto world, the bear is currently partying without restraint. In recent years, bitcoin has often been touted as the new or digital gold. But this year has shown that cryptocurrencies offer no protection against falling equity prices. Since the high in November 2021, the price has crashed by a massive 74%. In the past, even higher setbacks of between 83% and 94% have occurred.

Taking a long-term perspective, the price is still clearly up despite the current setback. Anyone wishing to invest in cryptocurrencies must be aware of the enormous fluctuations or even a possible total loss. Investments in crypto are a “gamble” and should be made only with “play money”. This type of investment is not suitable for diversification in the context of a portfolio, however, due to the extreme volatility.