Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Economy

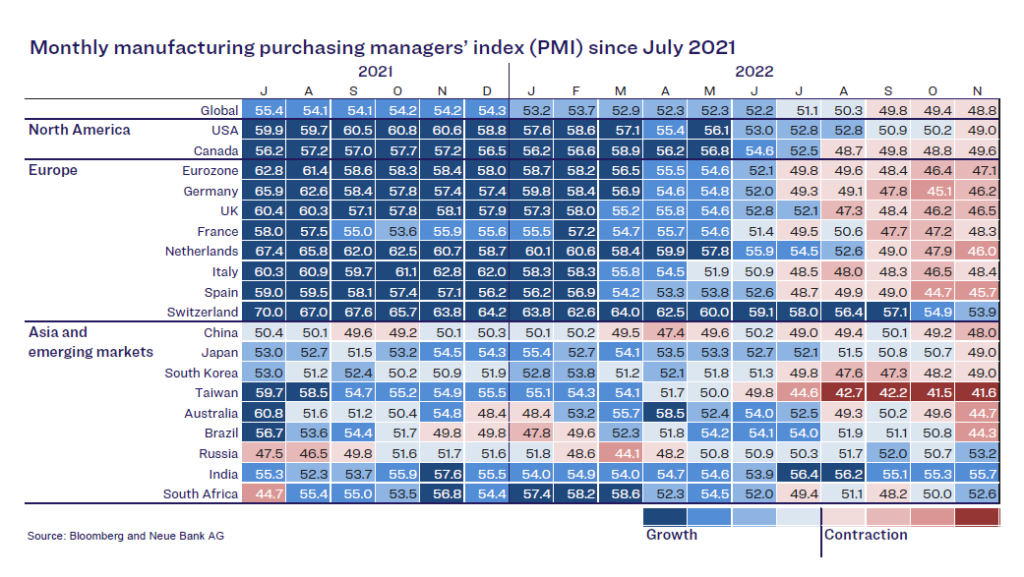

The majority of economists expect a recession for Europe and the United States in the first quarter of 2023. There is no consensus on the strength of the downturn, however, i.e. whether there will be a recession or just a “recessionette”. The chart below shows the development of the manufacturing purchasing managers’ indices (PMI). From August 2021 to November 2022, these leading indicators have weakened from strong growth (dark blue) into contraction territory (light red):

This data is still pointing to a rather mild weakening of the economy. The US labour market continues to show hardly any signs of weakness. Initial jobless claims and the unemployment rate are still at historically low levels. The data should be interpreted cautiously, however, given that it depicts only a glimpse of the past and is not a leading indicator like the PMI. Especially in the United States – where hardly any laws govern layoffs – these figures may deteriorate significantly in a very short time during an economic downturn. Our economic indicator – which has been signalling a possible recession since 20 July 2022 – has fallen further and is now signalling a more severe economic slowdown.

Equities

US consumer prices declined for the second month in a row. Headline inflation fell from 7.7% to 7.1% and core inflation from 6.3% to 6.0%. The improved inflation data, together with signs of a weakening economy, have allowed the US Federal Reserve (Fed) to slow its pace of interest rate hikes. This hope has been the driver of stronger equity markets over the past two months. We are sceptical about whether the recovery will continue, given that a recessionary trend is usually accompanied by a slump in corporate earnings. During a recession, the earnings of companies in the S&P 500 have declined by 20% on average. Currently, analysts are expecting a decline of 1.6% for the fourth quarter of 2022. The following example shows how far off experts’ estimates can be: At the beginning of 2008, earnings growth of 10% to 15% was expected. But the financial crisis intervened, and earnings plunged 92% from December 2007 to June 2009.

If there is a hard landing in 2023, corporate earnings are likely to slump more than analysts’ estimates.

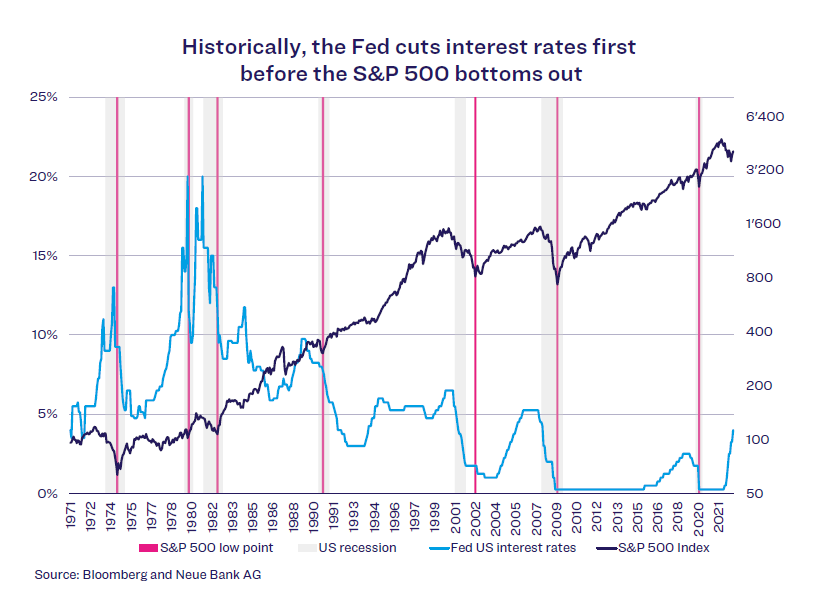

If that is the case, it would be questionable whether we have already seen the bottom of the equity markets. Moreover – as the chart below shows – following a cycle of interest rate hikes, the equity market only bottomed out after the Fed started cutting interest rates again:

The Neue Bank traffic light is also not signalling an all-clear for now, but rather remains at bearish (orange). For this reason, we are maintaining the partial hedging of our equity exposure.

Bonds

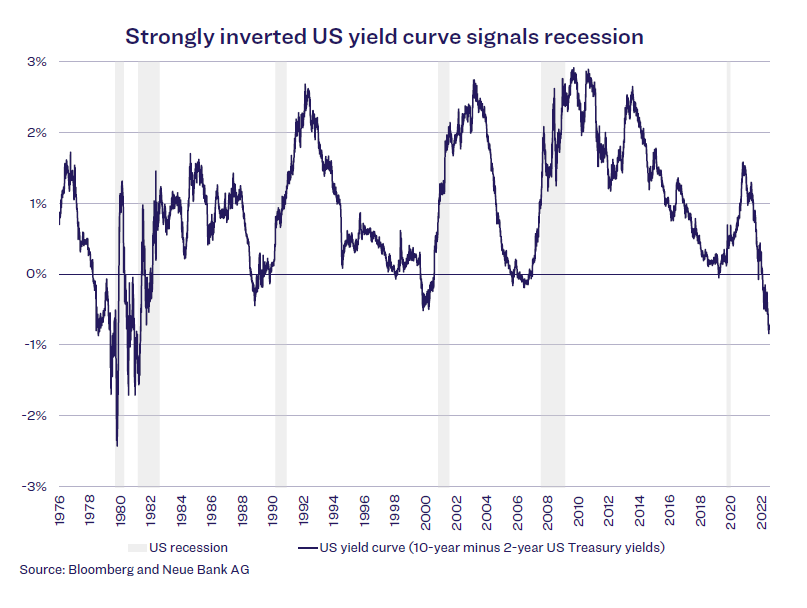

As the following chart shows, the last time the difference between yields on 10-year and 2-year US Treasuries was so clearly negative was in the early 1980s:

This means the US yield curve has become strongly inverted. In the past, this has always been a good indicator of an imminent contraction of the economy. Given the unambiguity of the signal, the bond market is now clearly indicating a recession. If this were to happen, yields on safe longterm government bonds would fall significantly. For this reason, we increased the duration of our portfolios in the reporting month using an ETF on long-term government bonds with the best credit ratings.

Currencies

The US dollar was unable to break through parity against the Swiss franc on a sustained basis. On the contrary, the USD/CHF fell from 1.01 to currently just under 0.93 since the beginning of November, which corresponds to a loss of about 8%. Our currency indicator helps to identify longer-term trends. The indicator is less suitable for quick and strong changes in direction. For this reason, the signal for the change in direction did not come until 5 December. Consequently, we hedged part of our USD positions in the CHF mandates and unwound the hedge in our USD mandates.

Alternative investments

Commodity price development can be used as an indication of the state of the economy. Rising oil prices, for example, indicate a growing economy, while strongly falling oil prices can be a sign of a weakening economy. At the beginning of June, the price of crude oil (WTI) was still over USD 120, but it has since fallen by 38% to USD 75. Despite the oil embargo against Russia, the price has continued to fall. This development could be a further sign of a cooling economy. Conclusion: Recession or “recessionette”? In our view, the indicators mentioned above tend to signal a more strongly weakening economy.