Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Alternative investments

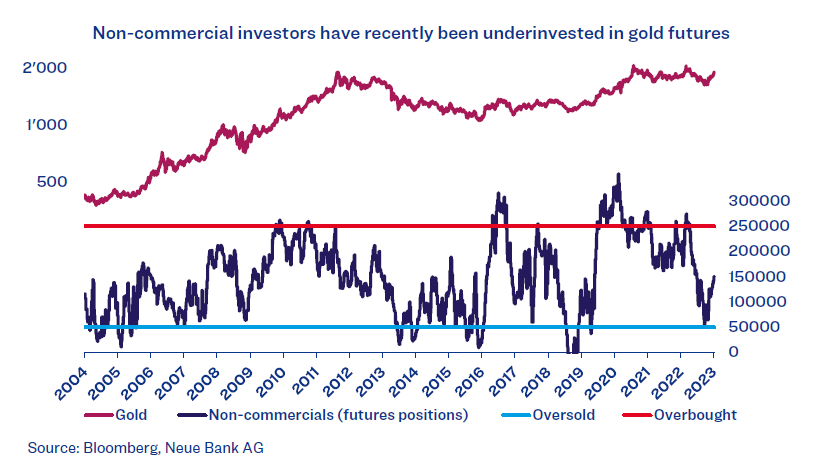

We have been invested in gold since the beginning of the month, once our momentum indicator for alternative investments gave a signal to that effect. Also during the reporting month, our trend indicator turned around and is now showing a positive price trend again.

These positive signals are supported by the preceding sharp decline in the positions of non-commercial investors in gold derivatives, which often signal the beginning of a change in trend. Following these technical measurements, one is naturally inclined to ask what the valuation looks like. We are not aware of any reasonable valuation methodology for gold. Former Fed Chairman Alan Greenspan has been quoted as saying, “The price of gold? That’s substance plus faith and fear minus interest.” Since this formula is likewise not resolvable, our assessment whether gold investments are attractive is limited to technical indicators.

Economy

The US Federal Reserve is still trying to win back trust and continues to signal a restrictive monetary policy. Implied interest rates show, however, that the market does not trust the Fed to pursue a sustained hawkish policy. Inflation is falling but still high, even though less attention is being paid to the latter fact at the moment. The labour market continues to exhibit low unemployment. The question remains whether there will be a recession and, if so, how severe it will be (see also Our Opinion of December 2022, “Recession or recessionette”).

Equities

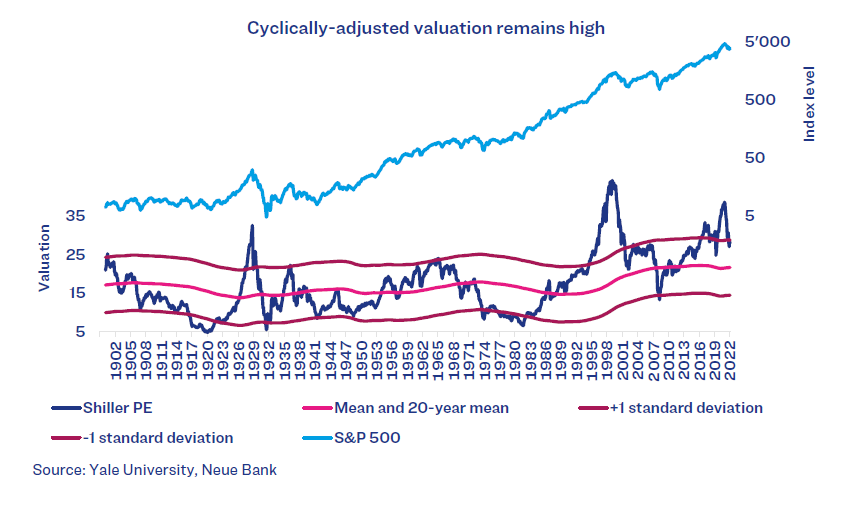

The equity market is rewarding the falling inflation data and pushing economic concerns into the background. Although equity prices corrected last year, cyclically-adjusted valuation (CAPE) is still high, historically speaking:

As the above chart shows, valuation has fallen at least somewhat from its highs, but it remains a standard deviation above the long-term mean. A high valuation is not a good timing indicator, however, and does not allow any conclusions about the near future. A continuation of the recovery that started in October can accordingly not be ruled out by any means.

„A high valuation is not a good timing indicator, however, and does not allow any conclusions about the near future.“

A trend reversal signal to that effect was given in January, which caused our traffic light to return to amber/yellow (neutral). The high valuation does allow us to draw one conclusion, however, namely that equity returns will be below average in the next decade. This correlation has been confirmed again and again in the past.

Bonds

In nominal terms, fixed-income investments are once again more attractive than in the recent past. Yields on first-class Swiss bonds have been mostly at 0% per year or below since 2014. Only over the course of the past year did yields climb back above zero and are now just over 1% per year. This has led to strong price losses on bonds, which could also not be cushioned due to the non-existent interest rates. The investment situation today is considerably better than it was a year ago, even though real interest rates are still clearly negative (due to high current inflation). Inflation has recently been falling, however, so that the risk of a sustained rise in interest rates appears limited.

Currencies

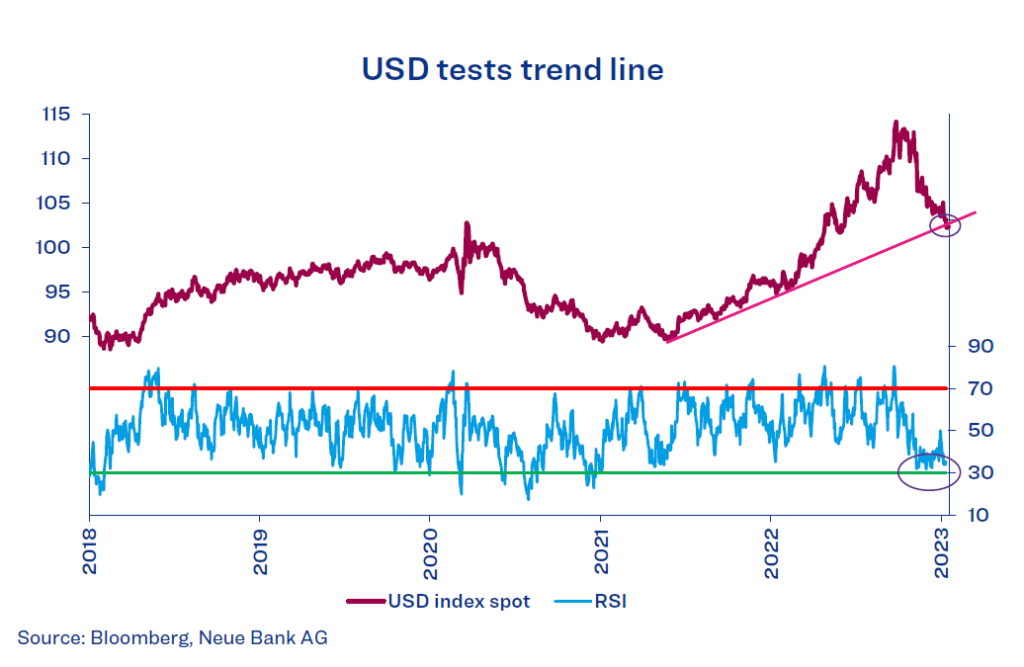

The USD index (calculated against a foreign currency basket of major currencies) has turned around and is now facing an important test of the trend line. Because of the oversold situation (measured by relative strength, RSI), a technical countermovement could follow in the short term.

If US inflation continues to ease, however, the risk appetite of investors could further increase. Assets parked in the safe haven of the USD would then flow back into other currencies, further weakening the greenback. We have meanwhile reduced the USD exposure in our CHF and EUR mandates.