Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Bonds

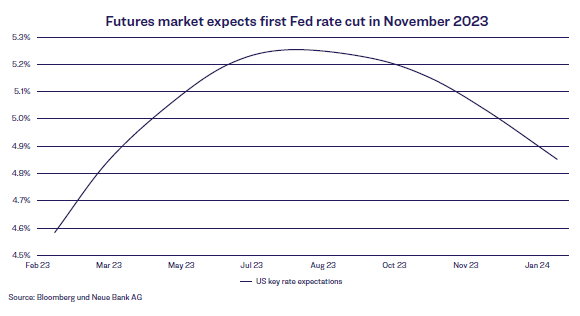

“Don’t fight the Fed”. This market adage should be followed not only during periods of loose monetary policy, but also when central bankers are raising interest rates significantly – as is currently the case. Right now, however, investors are not really trusting Fed Chairman Jerome Powell’s statements and are challenging the Fed – in line with the opposing motto: “Fight the Fed”. While Powell is trying to prepare market participants for further rate increases and a subsequent prolonged stay at that level, investors are expecting interest rate cuts already this year. The following chart shows the interest rate expectations for the key US rate traded on derivatives markets: Since this formula is likewise not resolvable, our assessment whether gold investments are attractive is limited to technical indicators.

The futures market is currently pricing in a 0.25% cut for the Fed meeting on 1 November 2023. But central banks are still walking a tightrope between inflation and recession. At this time, they can neither assume that inflation will be overcome nor rule out a recession. Despite this, investors believe that central banks will bring inflation under control without triggering a recession. If this is true, the potential for further yield increases will remain limited for the time being. We likewise do not believe yields will jump too much higher, and we recommend buying bonds with good credit ratings. If there is in fact a recession, safe bonds would benefit due to falling yields.

Equities

Equity market investors are also fighting the Fed. Despite restrictive monetary policy and the continuing risks of inflation and recession, confidence is currently dominating on the equity markets. The economic recovery in China after the end of its zero-Covid strategy, the averted energy crisis in Europe for now, and falling inflation rates worldwide have pushed fears of recession into the background, helping the markets to a brilliant start to the year. After only one and a half months, the MSCI World Index is already up by more than 8% in USD. This optimism

has also had an impact on the Neue Bank traffic light. On 23 January 2023, the trend indicators included in our traffic light turned positive, prompting us to completely unwind our partial hedge on equities. The Neue Bank traffic light is now at yellow/amber, corresponding to a neutral alignment of risk assets.

Looking back at the traffic light signals for the 2022 investment year, they turned out to be unsatisfactory and did not bring the desired success: hedging of equities was signalled too late. Because of our very active approach, this unfortunately cannot always be avoided, so the signals should be seen in a longer context. In the past, the traffic light has generated very good signals to reduce risks, especially in the event of major setbacks, so that asset losses relative to the overall market were lower.

“We continue to rely consistently on our Neue Bank traffic light; despite short-term setbacks, it’s important to stick to one’s strategy.”

Economy

US retail sales likewise started the year surprisingly strongly. Following the decline in December, retail sales were up 3% in January – the strongest increase since March 2021. US household sentiment has continued to improve in light of declining inflation and a still-solid labour market. Because consumers account for the largest share of US GDP, the US economy should be off to a good start in the new year. On the other hand, key global leading indicators still point to economic contraction. At 49.8 points, the global purchasing managers’ index remained slightly below the growth threshold of 50 for the sixth month in a row. Our economic indicator is also still signalling a recession, but it recovered significantly over the course of the reporting month. Based on the current data, the economy in Europe and the US might avoid the iceberg of a recession.

Currencies

Currency risks are often underestimated. They add to the risk of an investment and can have a significant impact on return. As an example: A Swiss investor wants to invest in USD bonds due to the higher interest rates. At the beginning of November 2022, the investor buys a 5-year USD bond with a yield of 4.5% for USD 10,000. At that time, the USD/CHF exchange rate was at parity, meaning that the investor had to pay CHF 10,000. About four months later, the USD/CHF rate is close to 0.93, which means that the USD bond is now worth only CHF 9,300. The investment has lost 7% in value, and its interest rate advantage has decreased significantly within a short period of time. Especially investors thinking in Swiss Francs have to act cautiously due to the strength of the CHF. For bonds, we always recommend hedging the foreign currency risks; for equity investments, we rely on our currency indicator, which signals whether to hedge or not to hedge. The indicator currently recommends hedging USD against CHF.

Alternative investments

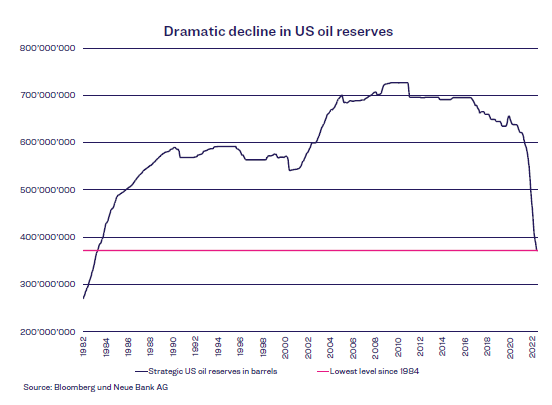

The International Energy Agency (IEA) expects global demand for crude oil to reach a record 102 million barrels per day in 2023. This means that supply is not expected to keep pace with stronger demand, even given a supply surplus of 1 million barrels per day at the beginning of the year. According to the IEA, the growing imbalance is expected to lead to higher oil prices especially in the second half of the year. The main factor cited is China’s hunger for energy, which will account for more than half of global demand following the end of its zero-Covid strategy. In our opinion, however, OECD countries are also likely to ramp up their demand significantly. In their fight against high energy prices, these countries have outright plundered their strategic oil reserves over the last two years. The US alone released an incredible 221 million barrels in 2022, causing its oil reserves to fall to their lowest level since 1984:

The plan is now to move in the other direction, and the US has already announced that it wants to fill its reserves again. But the US will certainly act with caution here, given that it wants to avoid an overly sharp rise in oil prices, which would lead to another increase in inflation.