Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Equities

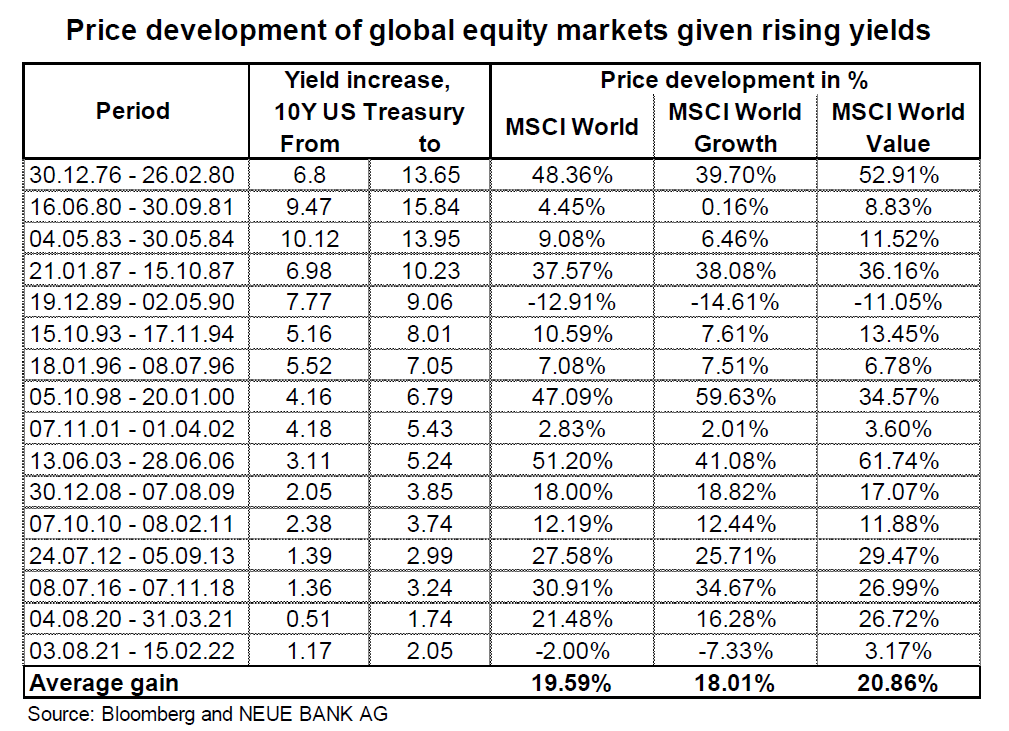

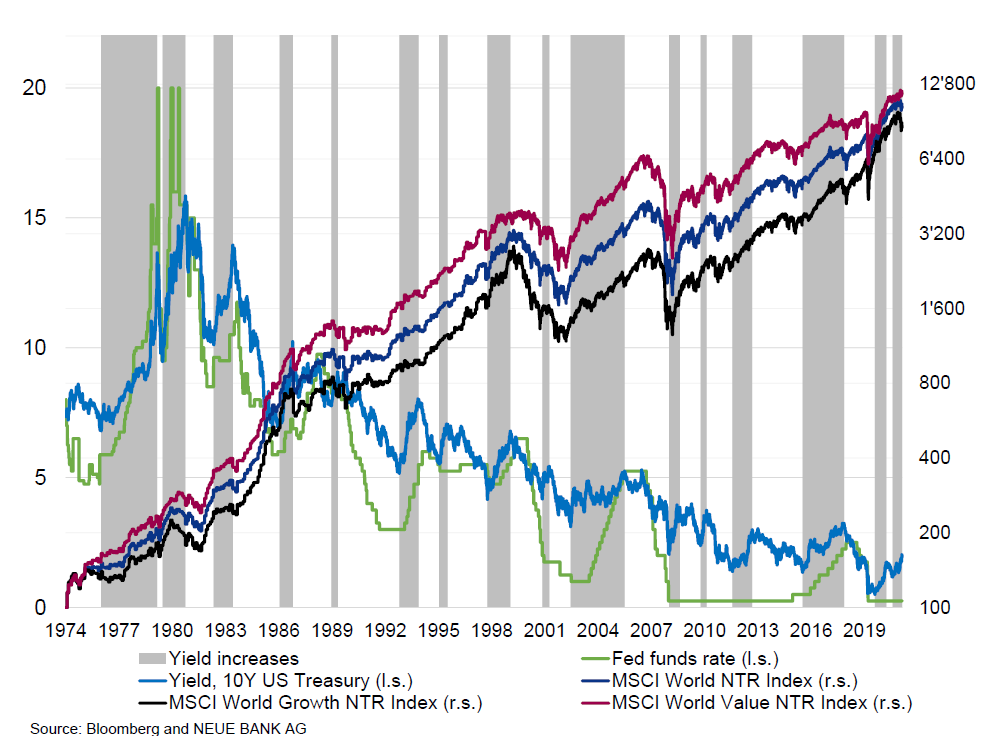

Most commentators appear to agree that rising interest rates weigh on the equity market. There is little historic evidence to that effect, however. On the contrary: historically, equity markets have usually risen when the US Federal Reserve (Fed) has raised interest rates, given that rate hikes are a clear sign of a strong economy. The following table and chart show the strongest increases in yields and the price development of the global equity market (MSCI World) over the past 46 years:

On average, the MSCI World Index gained 19.59% over all observed periods. Only at the beginning of the 90s and now is the world equity index in negative territory – but note that the current cycle of interest rate hikes is only just beginning. Typically, that is precisely when investors are most uncertain, leading to increased volatility on the markets. In the past, it was only once the central bank announced an approximate interest rate hike timetable that the equity markets calmed down. Major corrections have only ever occurred when the Fed has raised interest rates for too long, too sharply, and the economy slowed down too much as a result. But rising interest rates also have an impact on equity valuations. Highly valued companies in particular – i.e., growth stocks – are affected more strongly by this, given that future cash flows are discounted at a higher interest rate, resulting in declining enterprise value. This effect is also seen in the majority of historical observations. In such phases, growth stocks have on average performed less well than undervalued companies (value stocks) (see table). This is also currently the case, and some growth stocks have suffered significant setbacks. However, we believe that the large growth stocks offer long-term value, which is why the current weakness should not be overrated. We have not made any changes to the NEUE BANK traffic light, which is why it remains at yellow (neutral).

Economy

The leading economic indicators have continued to weaken, but some are still significantly above the growth threshold. Robust economic growth can therefore be expected in the coming months as well. The persistently high inflation data could now become a burden. In both the USA and Europe, there is no relief in sight in terms of price increases, and the central banks are increasingly coming under pressure to adjust their monetary policy.

Bonds

The financial markets are meanwhile expecting the Fed to increase interest rates up to seven times this year. Accordingly, yields have once again risen significantly. For example, the yield on 10-year US Treasuries has climbed above the 2% mark and is thus higher than before the start of the pandemic. In the wake of US yields, practically all bond markets have seen a strong rise in interest rates since the beginning of the year and consequently a fall in bond prices. We remain underweight in both exposure and maturities.

Currencies

The EUR/CHF exchange rate is moving closer and closer to parity. Despite this, the Swiss National Bank (SNB) has so far held back on buying foreign currencies and is no longer speaking of an overvalued Swiss franc. Why the change in opinion? First, the strong franc helps to dampen the inflationary surge from abroad, and second, the different inflationary developments at home and abroad play a role. In nominal terms, the CHF has appreciated significantly against the EUR (+13% since the minimum exchange rate policy was lifted at the beginning of 2015). In real terms, however, the picture looks different: Given that inflation in Switzerland is significantly lower than abroad, the Swiss franc has appreciated by only about 1% over the same period. Economists argue that real exchange rate developments are crucial for a country’s competitiveness, which is why Switzerland does not have to fear any major losses in its competitive position in the current environment. Our indicator also currently points to no firm EUR, which is why we are maintaining our partial hedging of EUR positions in our CHF mandates.

Alternative investments

Since the coronavirus shock, global bottlenecks have caused commodity prices to rise strongly. The futures curves on several markets are showing clear backwardation. This means that commodity traders have to pay significantly higher prices for immediate deliveries than for deliveries in the future. This price structure is seen as a sign of a pronounced undersupply in the commodity market. The Bloomberg Commodity Index – which tracks the prices of 23 commodity futures

– rose to a record level in the reporting month. This also had an impact on our momentum approach, which indicated a switch from listed private equity to commodities. We implemented this signal by purchasing a broadly diversified commodity ETF in our mandates on February 1.