Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Economy

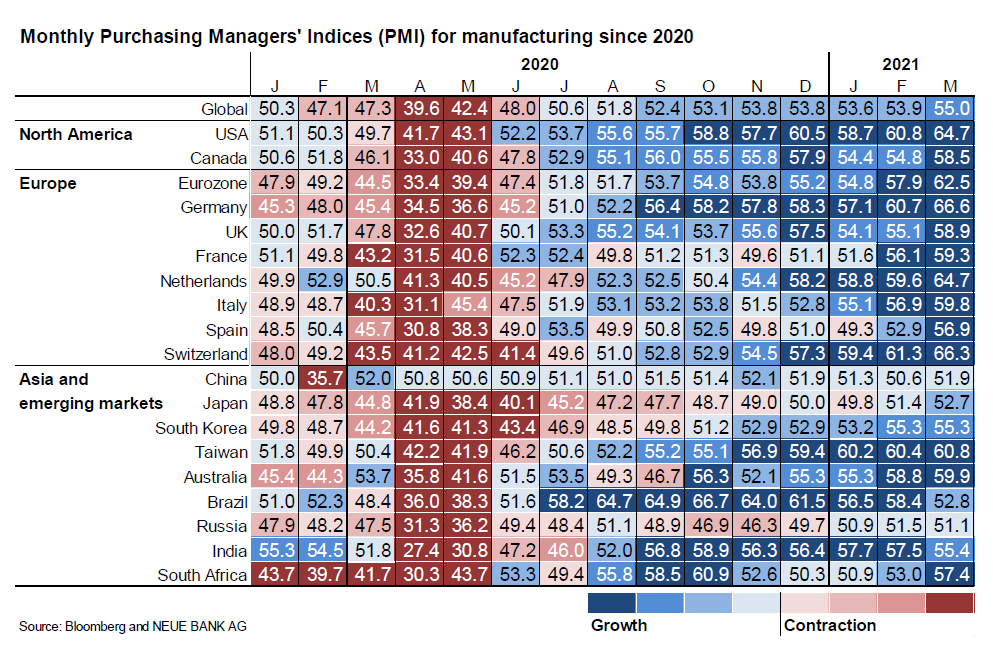

Current economic data around the globe points to a continued strong economic recovery, which could even lead to a boom over the course of the year. The most important leading indicators such as the Purchasing Managers’ Indices support these expectations. In the United States, the ISM Manufacturing index rose to 64.7 points, its highest level in 37 years. At 62.5 points, the Eurozone even reached its best result since the survey began 24 years ago. But also in other major economies, many of the values clearly exceed the growth threshold of 50, as the following table illustrates:

The current upswing is also being driven by consumers. In the US in particular, there was a veritable consumption boom in March. Retail sales rose by 9.8% and are an impressive 17.1% above the level before the coronavirus crisis in February 2020. Direct payments to US citizens out of the USD 1.9 trillion stimulus package and the gradual reopening of the economy contributed to the increase. In Europe, retail sales also exceeded expectations, but were significantly lower than in the US, rising by 3%. As vaccinations increase along with further easing of restrictions, consumers should continue to contribute significantly to the recovery of the economy in the coming months. This is why we view the current economic situation positively and expect the global economy to continue its V-shaped recovery.

Equities

Bulls kept the upper hand in the major equities markets in the month under review, and record highs were reached again in both the US and Europe. This rush to buy is triggered by investor optimism about growth due to the strong economic data, along with the promise of the major central banks to continue their ultra-loose monetary policy for a long time to come and the prospect of a USD 2.3 trillion infrastructure package in the US. This optimism is also reflected in the consensus estimates for corporate earnings growth in the S&P 500, which is expected to be 30.2% year-on-year in the first quarter – the highest earnings growth rate since the third quarter of 2010.

“This positive outlook – economic growth, monetary and fiscal policy, and rising earnings – continue to point to friendly equity markets.”

Significant growth is also expected for the rest of the year. If these assumptions turn out to be true, the corporate earnings in the S&P 500 would already be higher again in 2021 than before the pandemic year 2020. This positive outlook – economic growth, monetary and fiscal policy, and rising earnings – continue to point to friendly equity markets. The NEUE BANK traffic light also confirms this picture and is still green, which is why we are maintaining our overweight in equities.

Bonds

The strong rise in long-term yields has recently stalled, and the yield on 10-year US government bonds has fallen from its high of 1.75% this year to 1.55%. Despite excellent economic data and rising inflation data, financial market participants apparently believe that inflationary pressures are only temporary and that inflation expectations will not rise too much more.

“But if an economic boom does occur, the rise in yields may very well be strong.”

Because of the strong economic recovery, we believe that yields should increase again in the coming months, albeit to a manageable extent. But if an economic boom does occur, the rise in yields may very well be strong. We remain cautious on bonds and are maintaining our underweight position.

Currencies

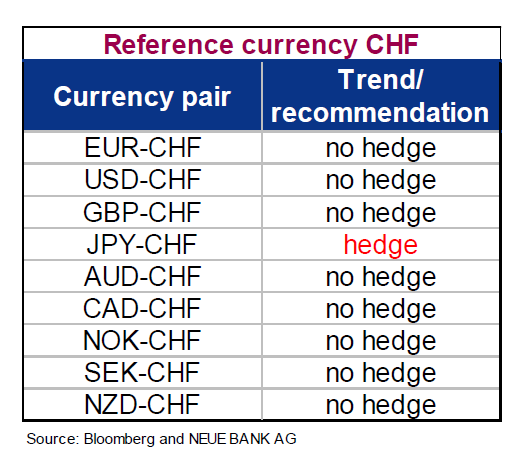

In times of economic recovery, safe haven currencies are increasingly sold off by market participants. This is currently evident in the Swiss franc, which has lost value against almost all major currencies since the beginning of the year. Our currency indicator also advises not to hedge the currencies listed in the chart against the CHF – with the exception of the JPY, given that the Yen is also a safe haven currency.

Alternative investments

At the beginning of April, our momentum indicator sent a new investment signal. We sold our commodities ETF with a gain of about 26% and took a new position in a listed private equity ETF. Listed private equity is not a direct investment in illiquid private equity capital, but rather an investment in listed companies that offer private equity investments primarily for institutional investors. Accordingly, our investment guarantees liquidity at all times.